Emergency Funds: Build your nest first

Written by: Clinton Graham

|

CFA, CFP

Published: Apr 07, 2026

Before you invest or buy a home, you need a buffer. An emergency fund is what keeps a difficult situation from becoming a financial crisis.

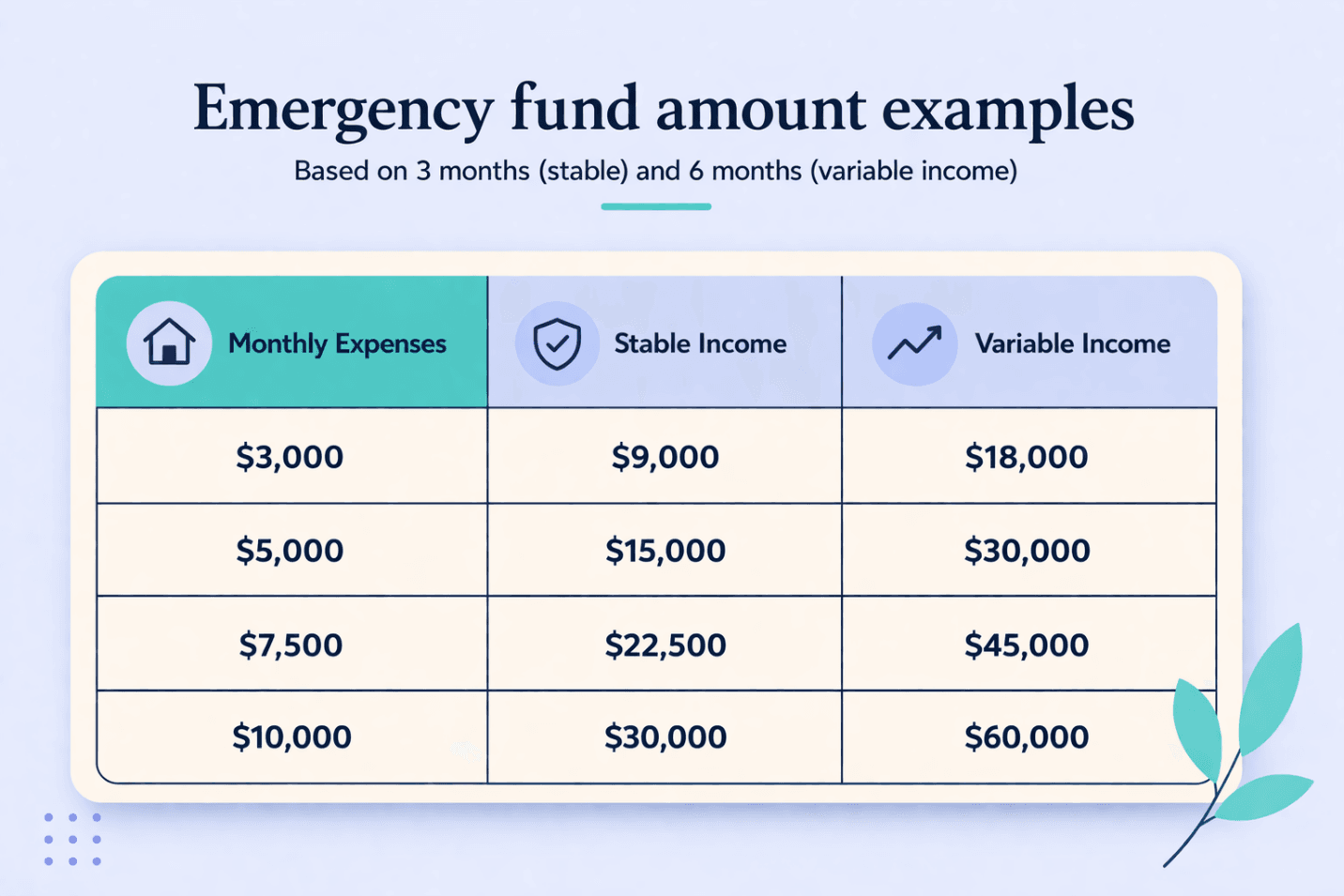

Investing without a cash cushion is like building a house on sand. It feels great until something shifts. When life throws a curveball, job loss, a blown transmission, or an unexpected medical bill, you can end up selling investments at the worst possible time, taking on high-interest debt, or putting your entire plan on hold. An emergency fund helps you avoid making those decisions under pressure. And in personal finance, decisions made under pressure are usually the most expensive ones. An emergency fund has one job: to protect you when something unexpected happens. It’s not for vacations, a new couch, or impulse purchases. It’s there for job loss, unexpected repairs, medical expenses, or urgent family situations. If you saw it coming, it’s not an emergency. You’ve probably heard the rule of thumb to keep three to six months of expenses saved. It’s a good starting point, but the better question is how long it would realistically take you to recover if your income stopped tomorrow. For some people, three months may be enough. For others, it’s not even close. You should lean toward at least six months or more if your income is variable, such as commission-based, self-employed, or contract work, if you work in a more volatile industry like tech startups, oil and gas, or real estate, or if you’re the primary income earner in your household. In those cases, your emergency fund isn’t just a cushion, it’s your runway. Give yourself enough of one.

An emergency fund doesn’t just protect your money. It protects your ability to stick to your plan.

Where you keep your emergency fund matters more than most people think. This money needs to be accessible and stable above all else. The goal isn’t to maximize return, it’s to make sure the money is there when you need it. The ideal place to store it is in a separate savings account where you can access it immediately through a transfer or ATM. Keeping it separate reduces the temptation to spend it and makes it clear that this money has a specific purpose. It can be tempting to chase higher returns by putting this money into an investment account, but that creates risk and delays access. If your emergency fund is invested, you may only be able to access it when markets are open, and even then, you could be dealing with settlement timelines and transfer delays. In a real emergency, you may need that money immediately, not in a few days. Your emergency fund should also be accessible to both partners if you’re in a household with shared finances. Holding this money in a joint account ensures that either person can access it when needed. In a true emergency, timing matters, and the last thing you want is for one person to be unable to access funds simply because the account is in the other person’s name. This becomes especially important in more serious situations, such as illness or loss of a partner. A joint structure removes friction and ensures the money is available when it’s needed most. There are also a few common mistakes to avoid. Don’t invest your emergency fund. If it can fluctuate in value, it’s no longer serving its purpose. Don’t keep it in your everyday chequing account either, where it can quietly disappear through small, frequent spending. It’s also best to avoid using your TFSA for this purpose. While it can technically hold cash, it’s better used as an investment account for long-term growth. Mixing the two can lead to inefficient use of your contribution room. An emergency fund isn’t exciting. It won’t show up in your returns or make for great dinner conversation. But once it’s in place, everything else becomes easier. Investing feels calmer, and big decisions feel more manageable. A strong financial plan doesn’t start with maximizing returns. It starts with making sure you’re protected when things don’t go as planned.