Retirement Plans Aren’t Enough on Their Own

Written by: Clinton Graham

|

CFA, CFP

Published: Apr 06, 2026

Retirement plans are one of the most valuable benefits employers offer. But on their own, they’re often not enough.

Many organizations invest heavily in retirement programs. Group RRSPs, pension plans, and matching contributions are designed to help employees build long-term financial security. These are valuable benefits, and they play an important role. But for many employees, they’re only part of the picture. Retirement plans are tools. They provide structure and incentives, but they don’t answer the broader questions employees are trying to solve. • How much should I be saving? • Am I on track? • Should I prioritize my RRSP or TFSA? • How does this fit with buying a home or paying down debt? Without context, even well-designed plans can be underutilized or misunderstood. Many employees contribute just enough to get the employer match, without fully understanding what that means for their long-term goals. Others may not participate at all, despite the benefit being available. In some cases, employees are making decisions that don’t align with their overall financial situation. Contributing to a retirement plan while carrying high-interest debt, or neglecting short-term savings, can create more stress rather than less. This isn’t a problem with the plan itself. It’s a gap in guidance. Retirement planning doesn’t happen in isolation. It’s connected to everything else. Cash flow, debt, savings, tax strategy, and life goals all influence how and when someone should be contributing. Without that broader view, employees are left to figure it out on their own.

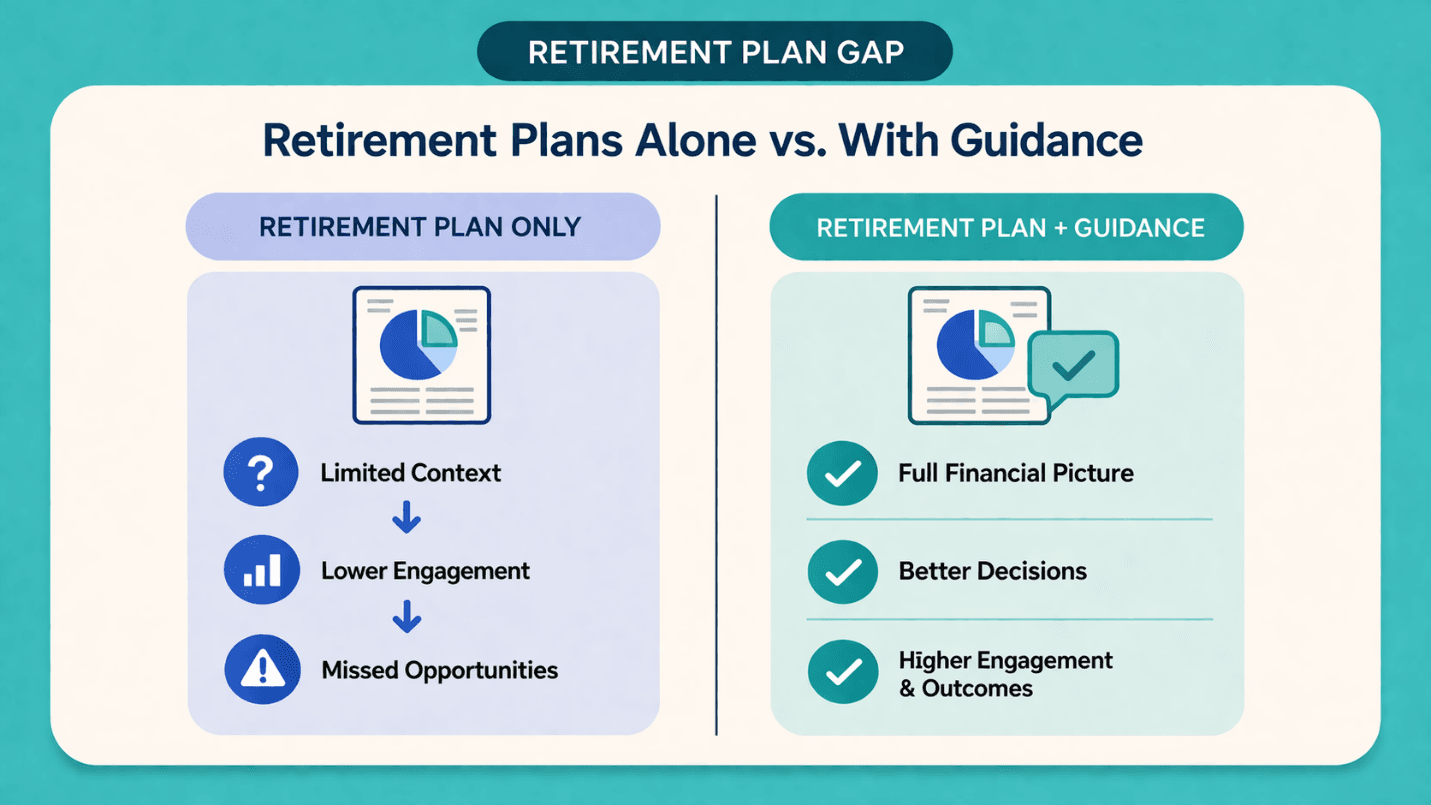

Retirement plans are powerful tools. But without guidance, they’re often underused.

Many retirement plan providers do offer support tools, such as fund selection guidance, asset allocation models, and retirement projections. These can be helpful, but they are typically focused on the plan itself. They don’t always take into account the full financial picture, such as debt, short-term savings, tax strategy, or competing priorities. It’s also important to recognize that these providers are primarily investment or insurance firms. Their guidance is often tied to the products and solutions they offer. That doesn’t make it wrong, but it does mean it may not always be fully independent or tailored to each individual’s broader situation. From an employer perspective, this creates a missed opportunity. Organizations are already investing in these programs. But without support to help employees understand and use them effectively, the full value isn’t being realized. Financial guidance helps connect the dots. It gives employees clarity on how their retirement plan fits into their overall financial picture. It helps them make informed decisions about contribution levels, account types, and priorities. It also increases engagement. When employees understand how a benefit works and how it applies to them, they’re more likely to participate and make better use of it. That improves outcomes without requiring additional investment from the employer. The goal isn’t to replace retirement plans. It’s to make them more effective by helping employees better understand and use the ones they already have. The value of a benefit isn’t just in offering it. It’s in how well it’s understood and used.